How Is Your Property Valued?

The Grafton Township Assessor determines the fair market value of all property within the township, including residential, commercial, industrial, farm, and vacant land.

The Illinois Department of Revenue defines fair market value as: “The most probable price a property would sell for in an open and competitive market, with a willing buyer and seller, both acting knowledgeably and without undue pressure, and allowing sufficient time for the sale.”

Under Illinois law, properties are assessed at 33⅓% of their market value. All property values are determined as of January 1of the tax year.

How Market Value Is Determined

The Assessor determines the assessed value used for property taxes by reviewing sales of homes similar to your property and comparing them to your home’s basic characteristics, such as size, age, location, and features. State law requires the Assessor to use sales from the three years prior to January 1 of the assessment year. For example, when valuing property as of January 1, 2026, sales from 2023, 2024, and 2025 are reviewed. This process reflects longer-term market trends and helps keep assessments fair and consistent across the township.

Reassessments and Ongoing Reviews

- General reassessment: Required by law every four years, when all properties are revised and corrected as needed.

- Ongoing reviews: The Assessor’s Office continually monitors all properties to maintain accuracy, fairness, and consistency. During these reviews, the Assessor may revise and correct assessments if property sales, market conditions, or verified information indicate a change is necessary.

Keeping Property Records Accurate

The Assessor’s Office maintains detailed records of each property’s characteristics, including size, construction type, and amenities.

Property changes are identified through:

- Building permits

- Neighborhood reviews

- Property Transfer Declarations (PTAX forms)

- Sales and Listing data

Accurate records help ensure all properties are valued fairly and that the property tax burden is distributed equitably across Grafton Township.

Features Considered in Determining Property Assessments

The following items are some of the features used to arrive at a determination of an assessed value.

- Square footage of the livable area

- Square footage of garages

- Basement or foundation type (slab, crawl, partial, full, walk-out)

- Central heating and air conditioning

- Plumbing fixtures (bathrooms, extra sinks)

- Open and enclosed porches

- Fireplaces

- In-ground pools

Features Not Considered

The Assessor's Office typically excludes the following items from consideration when determining assessed values. these items either add little to no measurable value compared to the property as a whole, are classified as personal property rather than real property, or do not impact the property's overall functional utility.

- Driveways, sidewalks, and driveway ribbons

- Landscaping, foliage, and retaining walls

- Privacy fences

- Garden sheds

- Above-ground hot tubs or pools

Why Do We Have Property Taxes?

Local property taxes fund essential services, including:

- Schools

- Police and fire protection

- Roads and infrastructure

- Libraries

- Parks and recreation

- City, village, and county services

Fair and equitable assessments ensure each property owner pays their appropriate share for the services they use.

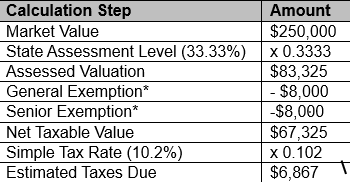

Assessed Value vs. Tax Bills

The assessor determines your property’s assessed value, but this does not directly determine your total taxes.

Your tax bill is calculated using the following formula

Assessed Value - Exemptions x Tax Rate = Tax Bill

The Assessor’s value is just one factor in determining your property taxes and does not directly set the total amount you pay. Your tax bill is calculated by applying the tax rate to your property’s assessed value, minus any applicable exemptions. The tax rate is based on the budget needs of the local government bodies each year. Even if property values go down, your taxes may still increase if taxing districts raise spending to maintain or expand services. See the included Property Tax Assessment and Billing Cycle graphic to understand the role of each department in the process. Click Here

*Exemptions vary; check with the assessor's office for eligibility.

Important Assessment Notice Update Effective 2026

Beginning in 2026, there will be an important change to how property assessment notices are delivered in McHenry County.

The Supervisor of Assessments will no longer mail assessment notices for properties that are only adjusted by the equalization factor.

What this means for you:

- These notices are still being created

- They are available online through the Tax Bill View lookup on the Treasurer's website: mchenryil.devnetwedge.com

- Use the link on the right-hand side to view your "Property Assessment Notice"

- You can access them any time once published

Notices WILL still be mailed for:

- Revaluations

- Farmland properties

- New Properties

Stay in the loop -- don't miss your notice.

Sign up for assessment alerts at: mchenrycountyil.gov/assessmentalerts

There, You'll find:

- Email/text notification signup

- A quick video on how to access your notice

- A direct link to DevNet Wedge

- Ongoing updates and helpful information

As always, our office is here to help. If you have questions or need assistance accessing your notice, please don't hesitate to reach out.

Your Rights and Responsibilities Filing an Appeal with the County Board of Review:

If you have questions or notice discrepancies regarding your property’s assessed value or characteristics, we encourage you to contact our office. My staff and I are happy to help you understand your property assessment and explain the assessment process. We aim to answer your questions and resolve concerns whenever possible. If, after speaking with our office, you are not satisfied with the outcome, you have the right to file an appeal with the McHenry County Board of Review. Appeals must be submitted within 30 days of the township’s publication date. For detailed information on the rules and procedures, complaint forms, filing deadlines, and more, please visit the McHenry County Board of Review website by clicking HERE

Supporting You and the Community We are here to help you understand your property assessment and how values are determined. Our office can provide guidance on available exemptions, assist with forms, answer your questions, and help guide you through the County Board of Review appeal process. We are committed to keeping assessments accurate and accessible, ensuring transparency and fairness for all residents of Grafton Township.

Looking for a convenient document that illustrates the Assessor's do's and don'ts? Please click HERE for a printout.

According to the Illinois Department of Revenue, the definition of market value is the "most probable sale price of property in terms of money in a competitive and open market, assuming that the buyer and seller are acting prudently and knowledgeably, allowing sufficient time for the sale, and assuming that the transaction is not affected by undue pressures".

The Illinois Property Tax Code states that property should be assessed at 33.33% of its fair cash value. All properties are valued as of January 1st of the tax year.

When determining the accuracy of value, the township assessor is required by law to consider sales over a three-year period prior to January 1st of the assessment year. A general reassessment is required every four years by law at which time all parcels are required to be reviewed and corrected as necessary. However, all areas of the township and sales are continually being monitored and studied. The job of Assessor is to keep a current record of property characteristics and sales data to ensure that all properties are accurately valued, allowing for a fair distribution of the property tax burden. Building permits, neighborhood reviews, and property transfer declarations (PTAX) are the primary sources of property information.

The assessor's office does not usually consider the following items when determining fair cash values. This is because the value contribution is negligible compared to the rest of the property's functional utility, the items are personal property, or the items are not considered real property.

- Driveways, sidewalks, and driveway ribbons

- Landscaping including foliage and related retaining walls, etc.

- Privacy fences

- Garden Sheds

- Above-ground hot tubs

- Above-ground pools

The following items are some of the features used to arrive at a determination of fair cash value.

- Square footage of the livable area of the property's improvements

- Square footage of the garage(s)

- Size and type of foundation (slab, crawl, partial, full, or walk-out)

- Central heating and air conditioning

- Plumbing fixtures (the number of bathroom fixtures and extra sinks)

- Open and enclosed porches

- Fireplaces

- In-ground pools

Local property taxes pay for such items as village, city and county services, schools, libraries, park districts, roads, fire and police protection. Equitable assessments ensure a fair distribution of the property tax burden among all property owners in the township who are allowed these services.

The Assessor's value does not solely determine the total amount of taxes collected but is only one variable in the calculation of your tax bill. The amount of taxes you pay is calculated by applying a tax rate to your property's assessed value, less any applicable exemptions. The tax rate is formulated based on how much the governmental bodies levy for their budget that particular year. Click HERE to refer to the Property Tax Assessment and Billing Cycle graphic to understand each department's role in the cycle.

If you have any questions or discrepancies about the value or chacteristics of your property, we encourage you to please call or visit our office to discuss your concerns. My staff and I will be glad to answer your questions or assist you in further understanding the assessment process. If you are not satisfied with our resolution, we will explain your option to appeal your value to the McHenry County Board of Review. Please access our Forms and Resources page for links to McHenry County forms and further information on the appeal process.

Looking for a convenient document that illustrates the Assessor's Do's and Don'ts? Please click HERE for a printout.

According to the Illinois Department of Revenue, the definition of market value is the "most probable sale price of property in terms of money in a competitive and open market, assuming that the buyer and seller are acting prudently and knowledgeably, allowing sufficient time for the sale, and assuming that the transaction is not affected by undue pressures".

The Illinois Property Tax Code states that property should be assessed at 33.33% of its fair cash value. All properties are valued as of January 1st of the tax year.

When determining the accuracy of value, the township assessor is required by law to consider sales over a three-year period prior to January 1st of the assessment year. A general reassessment is required every four years by law at which time all parcels are required to be reviewed and corrected as necessary. However, all areas of the township and sales are continually being monitored and studied. The job of Assessor is to keep a current record of property characteristics and sales data to ensure that all properties are accurately valued, allowing for a fair distribution of the property tax burden. Building permits, neighborhood reviews, and property transfer declarations (PTAX) are the primary sources of property information.

The assessor's office does not usually consider the following items when determining fair cash values. This is because the value contribution is negligible compared to the rest of the property's functional utility, the items are personal property, or the items are not considered real property.

- Driveways, sidewalks, and driveway ribbons

- Landscaping including foliage and related retaining walls, etc.

- Privacy fences

- Garden Sheds

- Above-ground hot tubs

- Above-ground pools

The following items are some of the features used to arrive at a determination of fair cash value.

- Square footage of the livable area of the property's improvements

- Square footage of the garage(s)

- Size and type of foundation (slab, crawl, partial, full, or walk-out)

- Central heating and air conditioning

- Plumbing fixtures (the number of bathroom fixtures and extra sinks)

- Open and enclosed porches

- Fireplaces

- In-ground pools

Local property taxes pay for such items as village, city and county services, schools, libraries, park districts, roads, fire and police protection. Equitable assessments ensure a fair distribution of the property tax burden among all property owners in the township who are allowed these services.

The Assessor's value does not solely determine the total amount of taxes collected but is only one variable in the calculation of your tax bill. The amount of taxes you pay is calculated by applying a tax rate to your property's assessed value, less any applicable exemptions. The tax rate is formulated based on how much the governmental bodies levy for their budget that particular year. Click HERE to refer to the Property Tax Assessment and Billing Cycle graphic to understand each department's role in the cycle.

If you have any questions or discrepancies about the value or chacteristics of your property, we encourage you to please call or visit our office to discuss your concerns. My staff and I will be glad to answer your questions or assist you in further understanding the assessment process. If you are not satisfied with our resolution, we will explain your option to appeal your value to the McHenry County Board of Review. Please access our Forms and Resources page for links to McHenry County forms and further information on the appeal process.

Looking for a convenient document that illustrates the Assessor's Do's and Don'ts? Please click HERE for a printout.